For decades, the Pakistani economy has been defined by a repetitive, exhausting cycle: borrowing to pay off old debts, followed by the “hat-in-hand” ritual of seeking rollovers from friendly nations. However, the recent decision to repay $3.5 billion to the United Arab Emirates (UAE) by the end of April 2026 marks a jarring, perhaps even courageous, departure from that script. While some may view this as a reckless drain on fragile foreign exchange reserves, I believe it represents a calculated gamble to reclaim national dignity and strategic autonomy in an increasingly polarized Middle East.

The End of the “Rollover” Leash

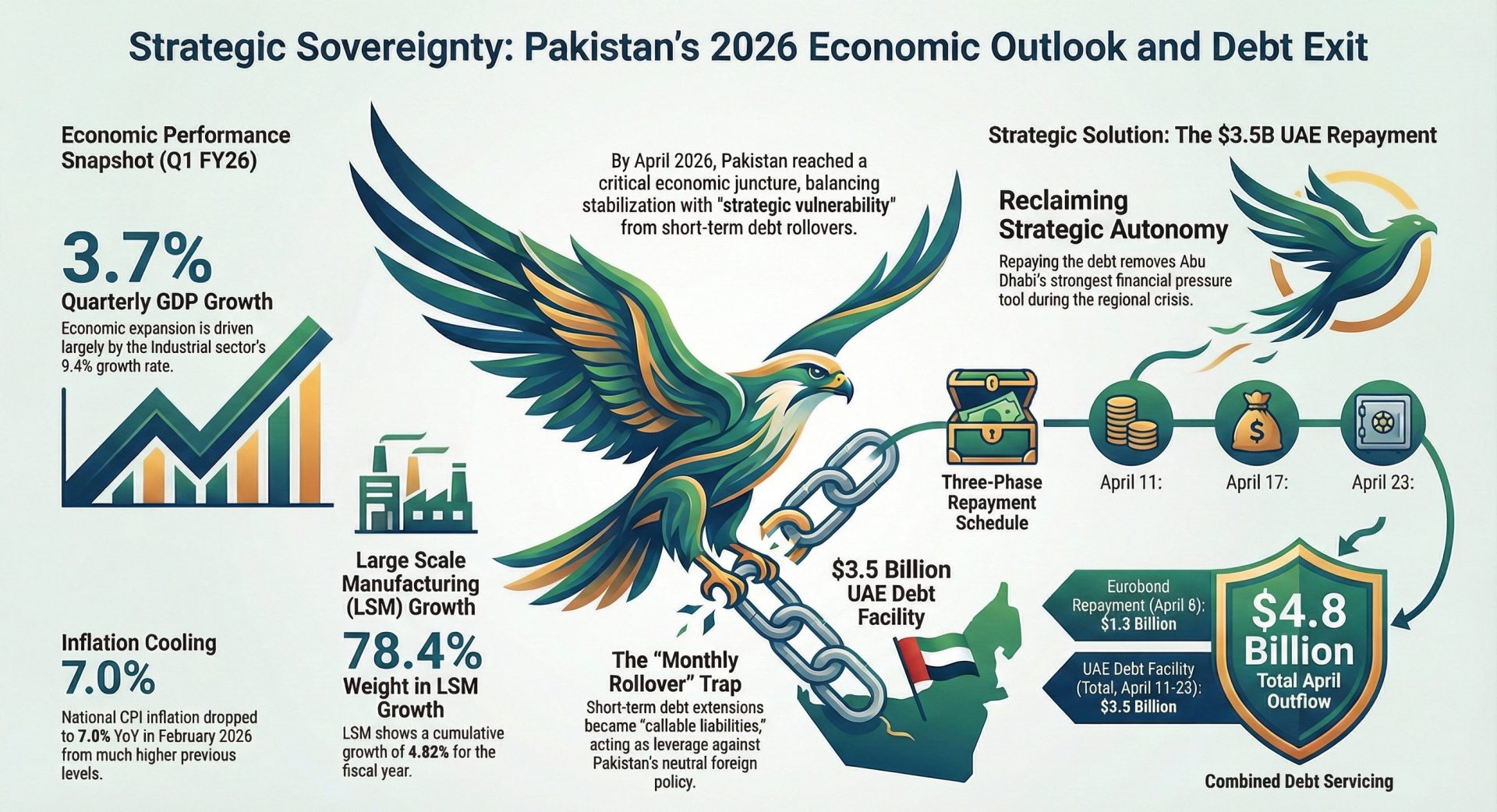

The timeline of these loans tells a story of long-term dependency. The package being returned includes a $2 billion deposit from 2018, a $1 billion loan from 2023, and—most remarkably—a $450 million loan dating back to 1996-97 that has been extended for nearly 30 years.

The UAE recently shifted its stance, moving from annual extensions to short-term monthly rollovers. This was not just a financial shift; it was a geopolitical one. As the Iran-United States conflict deepens, Gulf capitals have increasingly expected alignment. By shortening the “leash,” Abu Dhabi converted financial support into a potential pressure mechanism. Choosing to repay the full amount now—$450 million on April 11, $2 billion on April 17, and $1 billion on April 23—is Islamabad’s way of saying that its neutrality is not for sale.

A Staggering Economic Cost

We cannot ignore the math: this is a painful choice. Pakistan’s foreign exchange reserves currently stand at approximately $16.3 billion to $16.4 billion. Repaying $3.5 billion will slash those reserves by nearly one-fifth (18%), significantly weakening the country’s import cover and buffer against external shocks. This comes at a time when the nation still needs roughly $18 billion by June 2026 to satisfy reserve targets linked to its IMF stabilization program.

The immediate fallout will likely include increased pressure on the rupee and higher sovereign borrowing costs. However, there is a certain “sovereign credibility” gained by clearing these liabilities. Callable deposits from foreign governments are often viewed by markets as “temporary support” rather than durable reserves because they can disappear the moment a political disagreement arises. By settling this debt, Pakistan is making its remaining reserve levels more transparent and less vulnerable to sudden external whims.

From Debt to Investment: The Better Path

The most promising aspect of this transition is the ongoing discussion to convert debt into long-term equity investment. Deputy Prime Minister Ishaq Dar has previously highlighted talks regarding the UAE acquiring shares in Pakistani companies, potentially linked to the Fauji Fertilizer Group.

This is the shift Pakistan desperately needs. Replacing politically sensitive emergency loans with investment in infrastructure, energy, and logistics creates mutual dependence rather than one-sided leverage. If the UAE moves from being a “lender of last resort” to a stakeholder in Pakistan’s industrial growth, it stabilizes the relationship for the long haul.

Is it risky? Absolutely. Is it necessary? In my opinion, yes. Pakistan cannot continue to navigate the treacherous waters of Middle Eastern geopolitics if its financial survival depends on the monthly approval of its neighbors.

The April 2026 repayment may be remembered as the moment Pakistan decided to redefine the boundaries between economic necessity and a sovereign foreign policy. It is an expensive lesson in “national dignity,” but it is a price worth paying if it finally breaks the chains of debt-driven diplomacy.